Do you want to know how to invest, but don’t know where to start? I believe that creating a portfolio of investments that ultimately generate income is vital to creating our best life. Portfolio income can free up time because we don’t have to work so many hours, or it can supplement and even one day replace our work related income.

Investments include assets such as property, shares (parts of businesses), precious metals, or good old cash in some form. These have a monetary value and may pay us some income.

So here begins a series of 5 blog posts over the next little while, to introduce the concept of how to invest intelligently and become a Savvy Investor.

Disclaimer: Please note this information is not intended to imply any recommendation or opinion about a financial product. It is educational information only and does not constitute any kind of financial product advice.

How to Invest Intelligently Steps 1 – 3

1. Be totally clear on your objective

Why would you want to be an investor? What would get you even thinking about how to invest?

It could be:

— The realisation that you might want or need to stop working one day, and that the Age Pension and Superannuation are not going to generate enough money for you to meet your needs, or to enjoy your freed up time.

— Finding life stressful and wishing you didn’t have to work so much. Wishing that you could be calmer, go slower, and stop to smell the roses much more frequently.

— You know others who have invested successfully, and are now living partially or totally off the proceeds of their investment assets, and you want to do the same.

But how and where do you start? What do you invest in, and for what reason?

I’m going to shortcut this hugely for you and reveal that there are really only 2 main investment objectives. They are:

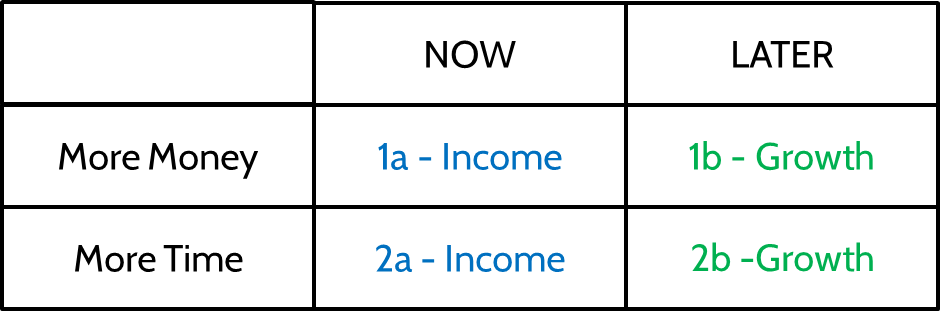

1. More money (more spending capability)

a. Now

b. Later

2. More time (less time spent working)

a. Now

b. Later

And as you can see, each of these is further split into whether that objective is a short term or long term objective.

Now of course we all want all of these four really don’t we?!

However, it is rare that any investment asset or strategy is a one size fits all kinda thing. So our question becomes “which one of these investment objectives do I want/need to focus on the most right now”?

LATER

If we consider the “later” option for money, we need to be definite about how far in the future we are thinking. The question to ask is “how much income am I likely to be earning in x years’ time?” Ask this for a range of 5 to 50 years. For each of those timeframes – will that be enough?

If we consider the “later” option for time, we need to be definite about how far in the future we are thinking. The question to ask is “how much time (not working) am I likely to be requiring in x years’ time?” Ask this for a range of 5 to 50 years. For each of those timeframes – will my income at that time be enough to allow that extra time off?

NOW

It’s a bit easier to consider what we need right now isn’t it. We can more easily answer whether we need/want more time, or more money, right now.

The next step is to prioritise those 4 options. Rate them 1-4 in order of highest (1) to lowest(4) need.

Now see where your number 1 fits on this chart:

Income means that the main objective of your investment is for money in your pocket. This is the YIELD, or ROI (return on investment as a percentage of the amount of money invested). Here you are looking for the highest percentage yield, and 15% looks way more attractive than 5%. (Beware of an important element of all investment strategies called RISK! This is a vital factor underlying the yield.)

Growth means that the main objective of your investment is for the VALUE of your asset to grow over time. In this case, income may not be a priority, or even be necessary. Imagine buying a $400k property that grows in value by 10% per year. It will be worth $800k in just 8 years. At 5% yield (return) this would earn you $20k per year…..

So what’s your objective? Is it Income (yield) or Growth right now?

2. Understand how much your desired lifestyle costs. (And why you need to understand this.)

The mouse-wheel that most are caught on is that of earning as much money as we can, and spending it all. There is always more we could spend, so we feel a constant sense of scarcity. This can propel us to either of these scenarios:

Investors who go crazy with their investing, even impoverishing their current lifestyles for the cause. They are caught in the “more” trap. They just want “more” assets, (maybe so they feel like they are financial hot-shots). You’ve heard about that amazing person who purchased 30 properties in 2 years? (You never did hear about how it all unravelled when they became overcommitted, and one card falling toppled the whole house.)

On the other hand, I’ve also met people who believe that they couldn’t possibly be investors because they don’t know enough, haven’t even got enough to live comfortably – let alone have anything left over to invest, or believe it’s some hugely complicated area that is beyond their capability.

In both these cases, the simple exercise of understanding how much their desired lifestyle actually costs brings INTELLIGENCE that inspires discovering how to invest. Most times I have been through this exercise with people they discover they don’t need the huge amount of extra income or assets they assumed. This can calm down overactivity, and boost underactivity.

Several of my program participants have been like Joanne and Ben. After looking at their figures and quantifying how they wanted their life to be, they realised they only need about $20,000 more per year, (rather than some nebulous huge amount) to be able to achieve their goal of annual world travel. This inspired them to take action and they completed a property flip that made them a good profit. Now they are on their way to working out how to do this consistently, as their chosen strategy for creating more money NOW. I would call this an Earnings Explosion Enterprise, rather than an Investment strategy, but the point is, that the knowledge of the numbers required for their desired lifestyle was what got them going to jump off the mouse wheel.

The pathway to understanding the cost of our desired lifestyle is to track and measure what our CURRENT lifestyle costs. When we get clearer on where our money is going, we realise where some wastage is, and where some wants are. You can work out how to track and measure yourself, or if you are someone who likes a guiding hand, My Savvy Investor Intensive ™ (online program) provides participants with templates and tools to accomplish this particular step.

3. Create a Cash Flow Surplus, and use the surplus to invest.

This is possible now that you have worked out where all your money is currently being spent!

After identifying some areas of wastage, and cutting down some expenses or discovering that you really do need to be earning more (and working out how to do that), you can also work out how much you could allocate regularly to be invested. It’s really as simple as that.

If you’re just starting out with learning how to invest, simply put a chosen amount into a separate bank account (that you call your wealth account, or investing account) on a regular basis. Watch it add up for a few months and then start having fun deciding where to invest it (see step 1 above!).

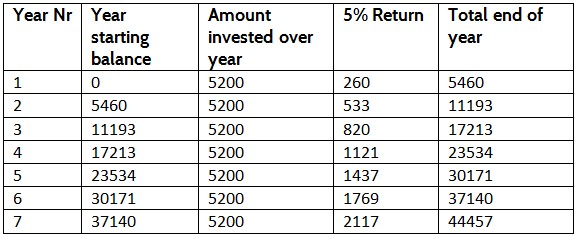

If you decided to invest $100 per week, here’s an idea of what you could achieve over time…..

You will have saved $5200 to be invested every year. This could be used to buy units in a fund, direct shares, shipping containers, gold or silver, or other relatively low-cost investments. Your choice will depend on your objective as covered in step 1

If you received a 5% return on your invested money each year:

Now at this stage you could possibly purchase a modest investment property, using the leverage of borrowed money. This is a double-edged sword, and you need to understand all the negatives as well as positives of this strategy. The positive outcome of this could be a $300k property that grows at 10% for another 5 years. Now you have a property worth $483k. Your loan is about $270k, so your equity (owned amount) is about $213k.

Now if you decided to use $100k of that equity, i.e. – borrow it at say 4% interest and invest that into an income generating investment that paid 15% per annum, you would be netting 11% which would be $11000 per year. Plus – you still own a property that is continuing to grow in value. This is after 12 years of just allocating $100 per week and making a smart GROWTH property purchase.

Hmmmm for many people that could mean they could almost work one day less per week, (have more time) or…..take a very fancy holiday every year….(have more money to spend).

This is just one very simple example of what is possible. There are loads of variations on this theme, and more factors to consider. But you have to know that this kind of outcome is very possible, in order to start putting away that $100 per week!

Well that’s a very long post about how to invest and become what I call a Savvy Investor, and there are several to come. Look out for parts 4 to 6 soon!

Wishing you Your Best Life,

Glenda